Top 10 Secrets to Picking the Best Health Insurance Plan in the USA for 2025

#401k2025 #RetirementPlanning #Maximize401k #FinancialFreedom #RetireRich #TaxHacks2025 #401kStrategies #PersonalFinance #RetirementGoals #MoneyTips

Are you ready to take control of your financial future in 2025? Whether you're starting your first job or approaching retirement, your 401(k) remains one of the most powerful tools to build wealth and enjoy a secure, comfortable future.

But here’s the deal: 2025 brings new rules, tax strategies, and investing opportunities—and understanding them could make a six-figure difference in your retirement savings.

In this guide, we break down 7 proven strategies that every American should follow to maximize their 401(k) in 2025. Whether you're aiming to retire early or simply want to optimize every dollar, this is your roadmap to smarter saving and investing.

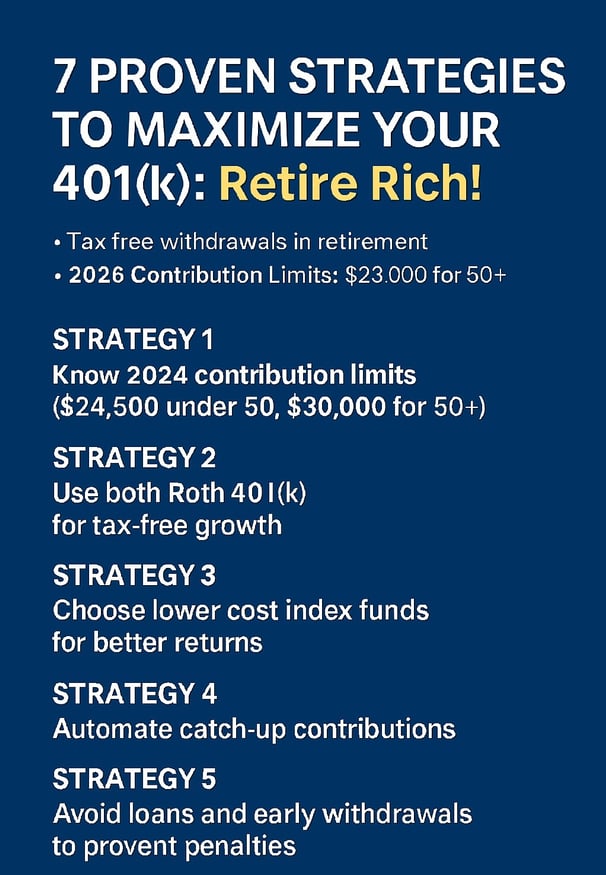

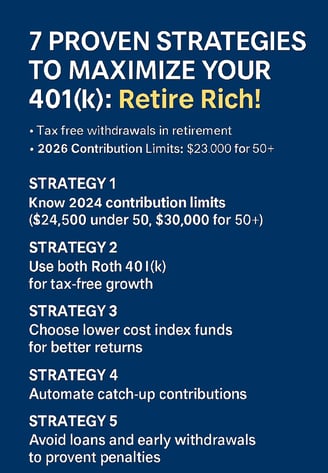

Strategy 1: Understand the 2025 401(k) Contribution Limits and Rules

The most fundamental step to maximizing your 401(k) is knowing how much you’re allowed to contribute—and what changes have occurred for 2025.

2025 Contribution Limits:

Under age 50: $23,500 (increased from $23,000 in 2024)

Age 50 and above: $31,000 (includes a $7,500 catch-up)

Solo 401(k) limit: Up to $69,000 (combined employee + employer contribution)

Why does this matter? The more you contribute, the more your money compounds tax-deferred. For instance, contributing the full $23,500 annually with an average 7% return could grow to over $1.2 million in 30 years.

Don’t Forget the Employer Match:

Many companies offer a 3–6% match. Not contributing enough to get this match is like walking away from free money.

Action Step:

Log into your 401(k) portal and check your current contribution.

Adjust it to meet the max if possible—or at least enough to get the full employer match.

If you’re self-employed, look into setting up a Solo 401(k), which gives you flexibility to contribute both as employee and employer.

Strategy 2: Leverage New 2025 Tax Hacks with Roth 401(k) Options

Thanks to the full rollout of the SECURE 2.0 Act, 2025 is a banner year for tax-saving opportunities through your 401(k).

Key Changes:

Roth 401(k) contributions are more accessible than ever.

Employers can now match into Roth 401(k)s.

You may qualify for a "Mega Backdoor Roth", which allows post-tax contributions that can later be converted into a Roth IRA.

Why It Matters:

Tax rates are likely to increase in the coming years, especially with expiring tax cuts from 2017. A Roth 401(k) lets you pay taxes now and enjoy tax-free withdrawals later—an incredible advantage if you expect to be in a higher tax bracket during retirement.

For example, if you invest $20,000 in a Roth 401(k) and it grows to $100,000, you pay zero tax on the $80,000 growth.

Action Step:

Ask your HR department if Roth contributions and matching are available.

Use a Roth vs. Traditional calculator to estimate future tax benefits.

If eligible, explore after-tax contributions and rollovers into a Roth IRA.

Strategy 3: Optimize Investment Choices Based on 2025 Trends

A 401(k) is not just a savings account—it’s an investment engine. Choosing the right funds can dramatically impact your returns.

Top 2025 Investment Themes:

Low-cost index funds (e.g., S&P 500, total market funds)

ESG funds (environmental, social, governance-focused)

Thematic ETFs in sectors like clean energy, healthcare innovation, and AI

The Fee Trap:

Many older plans still push actively managed funds with 1–2% fees, which can cost you hundreds of thousands of dollars over time. Aim for funds with expense ratios below 0.5%—ideally under 0.2%.

Action Step:

Log into your plan and view your current investment allocations.

Reallocate toward diversified, low-fee funds that match your risk level.

Rebalance your portfolio at least once a year or when market changes occur.

Strategy 4: Automate Contributions for Consistent Growth

Consistency is king when it comes to saving for retirement.

Benefits of Automation:

Payroll deductions ensure consistent investing.

Auto-escalation features increase your contribution by 1% annually—pain-free.

Dollar-cost averaging helps manage market volatility by investing at regular intervals.

A small increase of just 1% annually can lead to thousands more in retirement savings without affecting your lifestyle significantly.

Action Step:

If not already automated, set up payroll deductions today.

Ask your HR if your plan offers auto-escalation.

Aim to contribute 10–15% of your income, including employer matches.

Strategy 5: Use Catch-Up Contributions and Special Rules After Age 50

2025 is particularly favorable for older workers.

Key Catch-Up Opportunities:

Ages 50+: Eligible for $7,500 in catch-up contributions

Ages 60–63: Eligible for "Super Catch-Up" of up to $10,000, indexed for inflation

Solo 401(k): Self-employed savers can go up to $69,000, plus catch-ups

Why It’s Crucial:

If you’re behind on retirement savings, these catch-up contributions allow you to turbocharge your efforts in the final working years.

Action Step:

Max out catch-up contributions if you’re 50 or older.

Self-employed? Consider a Solo 401(k) through providers like Vanguard, Fidelity, or Charles Schwab.

Strategy 6: Avoid Common and Costly 401(k) Mistakes

Even seasoned investors make errors that jeopardize retirement goals.

Common Pitfalls to Avoid:

1. Early Withdrawals: Taking money out before age 59½ triggers a 10% penalty plus taxes.

2. 401(k) Loans: Even if you repay them, you lose out on potential investment gains.

3. Neglecting Old Accounts: Leaving behind an old 401(k) at a past job? You may be stuck with high fees and limited options.

4. Forgetting Beneficiaries: Life changes like marriage or divorce? Update your forms—outdated designations can cause serious legal headaches.

Action Step:

If you’ve changed jobs, roll over old accounts into a low-cost IRA or your current plan.

Review beneficiary designations annually.

Avoid loans unless it’s an absolute emergency—and have a repayment plan if you already borrowed.

Strategy 7: Plan for New Regulatory Changes and Your Long-Term Retirement Goals

2025 introduces some sweeping regulatory shifts—be ready to adapt.

Key Regulatory Updates:

Mandatory Auto-Enrollment: New employer-sponsored plans must auto-enroll employees.

Emergency Savings Within 401(k)s: Withdraw up to $1,000 without penalty for urgent needs.

RMDs: Required Minimum Distributions now start at age 73 (may increase further in coming years).

Aligning with Your Retirement Goals:

Experts recommend saving 10–12x your final salary to retire comfortably. Use retirement calculators to see where you stand. For example, if your final salary is $90,000, your target nest egg should be $900,000–$1.08 million.

Action Step:

Use a tool like SmartAsset or Fidelity’s retirement calculator.

Check if your 401(k) supports emergency savings features.

Consider a fiduciary advisor to help you plan for distributions, taxes, and legacy planning.

Final Thoughts: Start Now, Retire Rich

Let’s recap the 7 strategies that can transform your retirement savings in 2025:

1. Know the 2025 contribution rules and limits

2. Leverage Roth 401(k) and other tax-saving hacks

3. Optimize your investment mix with low-cost funds and trends

4. Automate contributions and use auto-escalation

5. Use catch-up rules if you’re 50+ or self-employed

6. Avoid early withdrawals, loans, and outdated beneficiaries

7. Plan ahead for new 2025 rules and align with long-term goals

Each step above could potentially add tens—or even hundreds—of thousands of dollars to your retirement fund.

Remember, the sooner you start optimizing, the better your future will look.

⚠️ Disclaimer:

This article is for informational purposes only and does not constitute financial, legal, or tax advice. Please consult a qualified financial advisor or tax professional before making investment decisions. All data is accurate as of June 2025, but rules and regulations may change.