Top 10 Secrets to Picking the Best Health Insurance Plan in the USA for 2025

Discover the top 10 secrets to choosing the best health insurance plan in the USA for 2025. Save money and get the coverage you need with our free course! Learn expert tips now.

Choosing a health insurance plan in the United States has always been a complex task, and in 2025, the challenge is greater than ever. With insurance premiums rising by an average of 7% this year, many Americans are reevaluating their options to find affordable, comprehensive coverage. This guide breaks down the key steps and considerations to help you make the best decision for your health and your wallet.

Key Highlights for 2025

Average premiums have increased by 7% — evaluating total costs is more important than ever.

Marketplace subsidies may change — especially later in 2025 due to expiring provisions from earlier stimulus packages.

Policy changes like Medicaid reductions could impact low-income households.

Healthcare.gov remains the best tool for comparing available plans and estimating costs.

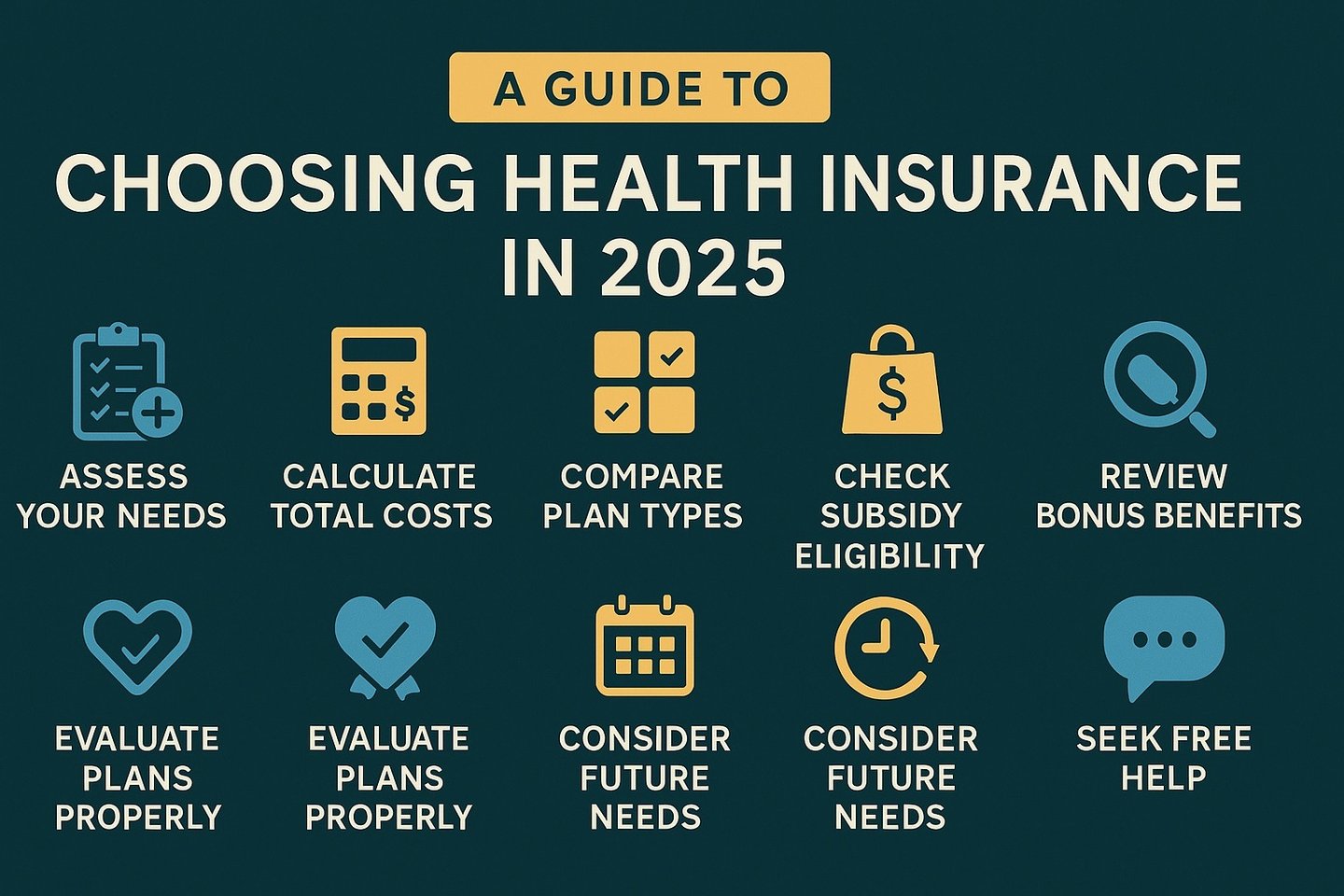

Step 1: Understand What You Need from Your Health Insurance

Start by assessing your personal or family healthcare needs. Think about the number of doctor visits, prescription medications, specialist consultations, or mental health services you expect to use.

In 2025, many insurers offer plans tailored to specific chronic conditions like diabetes or cardiovascular issues. These can be highly cost-effective if they match your needs.

Also, verify that your preferred doctors and hospitals are in-network to avoid hefty out-of-network charges—particularly relevant this year due to network shrinkage from insurance market consolidation.

Step 2: Get a Handle on the Total Cost

While your monthly premium is the most visible cost, don't ignore the hidden ones:

Deductibles: What you pay before your insurance kicks in.

Copays & Coinsurance: The portion of medical bills you share after reaching your deductible.

Out-of-pocket Maximums: The absolute limit you'll pay before insurance covers 100% of covered services.

Pro Tip: Use the cost calculator on HealthCare.gov to compare these amounts based on your expected healthcare usage. A lower premium might look appealing, but it can hide higher deductibles or copays.

Step 3: Know Your Coverage Options

In 2025, the main types of plans still include:

HMO (Health Maintenance Organization) – lower cost, requires referrals.

PPO (Preferred Provider Organization) – more flexible, higher premiums.

EPO (Exclusive Provider Organization) – no referrals, but limited networks.

POS (Point of Service) – hybrid with some out-of-network options.

Each comes with trade-offs in flexibility, cost, and network size. Plans are also grouped into metal tiers (Bronze, Silver, Gold, Platinum), representing the ratio of premium costs to out-of-pocket expenses.

Step 4: Check Your Eligibility for Subsidies

Subsidies can significantly reduce monthly premiums for qualifying households. These are based on your income and household size.

⚠️ Important: Some subsidy expansions introduced in prior years may begin phasing out in late 2025, so double-check your eligibility during enrollment.

Visit HealthCare.gov and use the eligibility tool to estimate your tax credits.

Step 5: Don’t Overlook Bonus Benefits

Some plans now offer non-traditional perks like:

Free telehealth consultations

Wellness incentives for meeting health goals

Gym memberships or fitness trackers

Dental and vision add-ons (especially in Medicare Advantage plans)

If you’re proactive about your health, these extras could make a big difference in both outcomes and cost.

Step 6: Scrutinize the Fine Print

Be aware of:

Exclusions: Services not covered at all

Prior Authorizations: Required approvals for procedures

Waiting Periods: Delays in coverage for certain services

In 2025, new regulations are designed to enhance transparency, but reviewing your Summary of Benefits and Coverage (SBC) remains essential.

Step 7: Compare Plans Correctly

Avoid mismatched comparisons. Compare:

Plans within the same metal tier

Network coverage for doctors, hospitals, and specialists

Total annual cost estimates based on your usage

Some providers, like Blue Cross Blue Shield, offer expansive nationwide networks, while others may be region-specific but more affordable.

Step 8: Consider Your Health and Future Plans

Are you expecting life changes like having a baby, surgery, or managing a chronic illness?

Families: Ensure pediatric and maternity care are covered.

Seniors: Evaluate Medicare Advantage plans, which may offer dental, vision, and hearing benefits.

Low-Income Individuals: With Medicaid eligibility redeterminations ongoing, you may need to switch to Marketplace coverage.

Plan not just for today—but for what the next 12 months could bring.

Step 9: Know When You Can Enroll

The open enrollment window for 2025 was November 1, 2024 to January 15, 2025.

Missed it? You might still qualify for a Special Enrollment Period (SEP) if you’ve had a major life event—like moving, losing coverage, or having a child.

Check HealthCare.gov for current SEP rules and timelines.

Step 10: Get Help—It’s Free!

Feeling overwhelmed? You're not alone.

Use navigators from non-profits who offer no-cost help.

Call the HealthCare.gov helpline for guidance.

Consider licensed insurance agents or brokers for more tailored advice.

A little expert help now can prevent costly mistakes later.

Smart Ways to Save on Health Insurance in 2025

Opt for High-Deductible Health Plans (HDHPs) with Health Savings Accounts (HSAs).

Take full advantage of wellness rewards programs offered by some insurers.

Compare, compare, compare—even a $30 monthly difference adds up to hundreds annually.

Estimate your 2025 income correctly for subsidy eligibility.

Step-by-Step Summary

1. Assess Your Health Needs

Think about your regular healthcare usage: prescriptions, check-ups, chronic conditions, or planned procedures.

2. Understand the Plan Types

Know the difference between HMO, PPO, EPO, and POS plans. Your flexibility and costs will vary by plan type.

3. Compare the Full Costs

Don’t just look at premiums. Consider deductibles, copays, coinsurance, and out-of-pocket maximums.

4. Use HealthCare.gov Tools

Leverage the plan comparison and subsidy estimator tools for accurate 2025 data.

5. Verify Provider Networks

Check if your doctors, hospitals, and specialists are in-network to avoid high out-of-pocket costs.

6. Apply for Financial Help

Review eligibility for premium tax credits and cost-sharing reductions. Some subsidies may expire by the end of 2025.

7. Evaluate Extra Benefits

Look for value-added features like telehealth, fitness incentives, vision/dental, or wellness perks.

8. Stay Informed About Changes

Be aware of policy changes (e.g., Medicaid eligibility redeterminations or subsidy rollbacks) that could affect your plan.

9. Seek Professional Help if Confused

Use certified navigators or licensed brokers for support. Open enrollment for 2025 is closed, but special enrollment may apply.

10. Plan for the Future

Choose a plan not just for today’s needs but for events like maternity care, aging parents, or expected surgeries.

Take Charge of Your Health Coverage

The health insurance landscape in 2025 is dynamic—but with the right strategy, you can find a plan that offers excellent coverage without breaking your budget.

Whether you’re selecting a new plan due to a life change or just reassessing your current coverage, now is the time to act. Use trusted platforms like HealthCare.gov, read the fine print, and seek help if needed.

Health insurance is more than a policy—it’s your safety net. Choose wisely.

Key Resources

Best Insurance Plans in 2025 – Forbes Advisor

Medicaid Enrollment and Marketplace Trends – McKinsey

Disclaimer:

This article is for informational purposes only and does not constitute financial, legal, or medical advice. Health insurance policies and government programs can change. Always consult with a licensed healthcare professional, insurance broker, or the official HealthCare.gov website for the most accurate and personalized information.